What Doing It Yourself Really Buys You

An honest look at what advice costs, what a good adviser is genuinely worth, and why the main benefit of running your own fund is the one most people overlook.

If you run your own super fund, you have already done something brave. You decided to manage your own money instead of handing it to someone else. Most people never do that. They give away the wheel and hope for the best.

You chose differently. So it is worth being clear about what that choice really gives you, because the usual answer is only a small part of the story.

Most people who go it alone are mainly trying to save on fees. That is a fair goal, and we will cover it. But it is not the biggest prize. The biggest prize never shows up on a bill, and by the end of this you will see why it matters more than the money ever could.

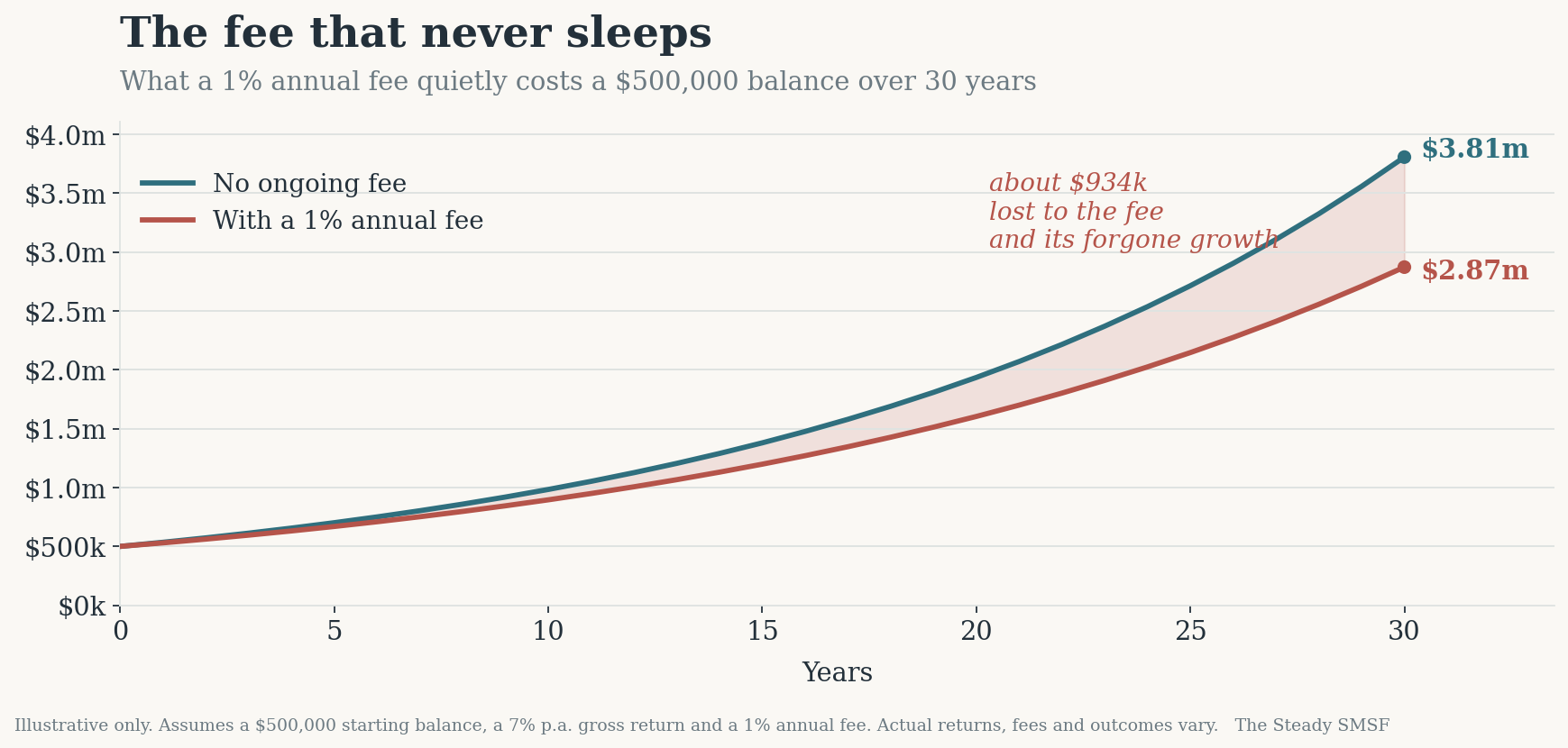

💸 The fee that never sleeps

In 2025, the median cost of ongoing financial advice in Australia was about $4,668 a year, according to the 2025 Australian Financial Advice Landscape report. That was up about 18 percent on the year before.

Many trustees pay between $3,500 and $15,000 a year. Where the fee is charged as a percentage of your balance, it is usually between 0.5 and 2 percent a year.

A flat dollar fee is easy to judge. It stays the same. A percentage fee is harder to see clearly, because it grows as your fund grows. It quietly takes more every year, even when the work has not changed.

Half a percent on a $400,000 balance is $2,000. The same half a percent on a $1.2 million balance is $6,000, for advice that might look identical.

And the fee does not just leave your account. It also takes away everything that money would have earned if you had kept it invested. So you pay it once, and then you pay it again in lost growth, every year, for as long as you hold the fund.

Over a lifetime, that is not small change. The chart above shows how a 1 percent fee could cost a $500,000 balance close to $934,000 over thirty years. That is most of a second fund, gone.

🪑 What a good adviser is genuinely worth

This is the part people skip when they get angry about fees. Skip it, and you end up with a cheap fund that is run badly.

A good adviser earns their fee in two places.

The first is the hard, one-off decision. A tricky pension or contribution strategy. Estate planning. Sorting out your money after a death, a divorce, or the sale of a business. Here, a single mistake can cost far more than years of fees, so paying once for real expertise is often money very well spent.

The second is harder to admit. A good adviser can stop you from doing something rash in a panic. When markets crash and every part of you wants to sell, the person who talks you out of it has just saved you more than years of fees. A lot of the value of advice was never the advice. It was the discipline.

So the fair view is not that advice is a rip-off. It is that advice is worth a lot for the hard parts, and worth very little for the part most people actually pay for: having someone hold a simple, low-cost portfolio they could easily hold themselves.

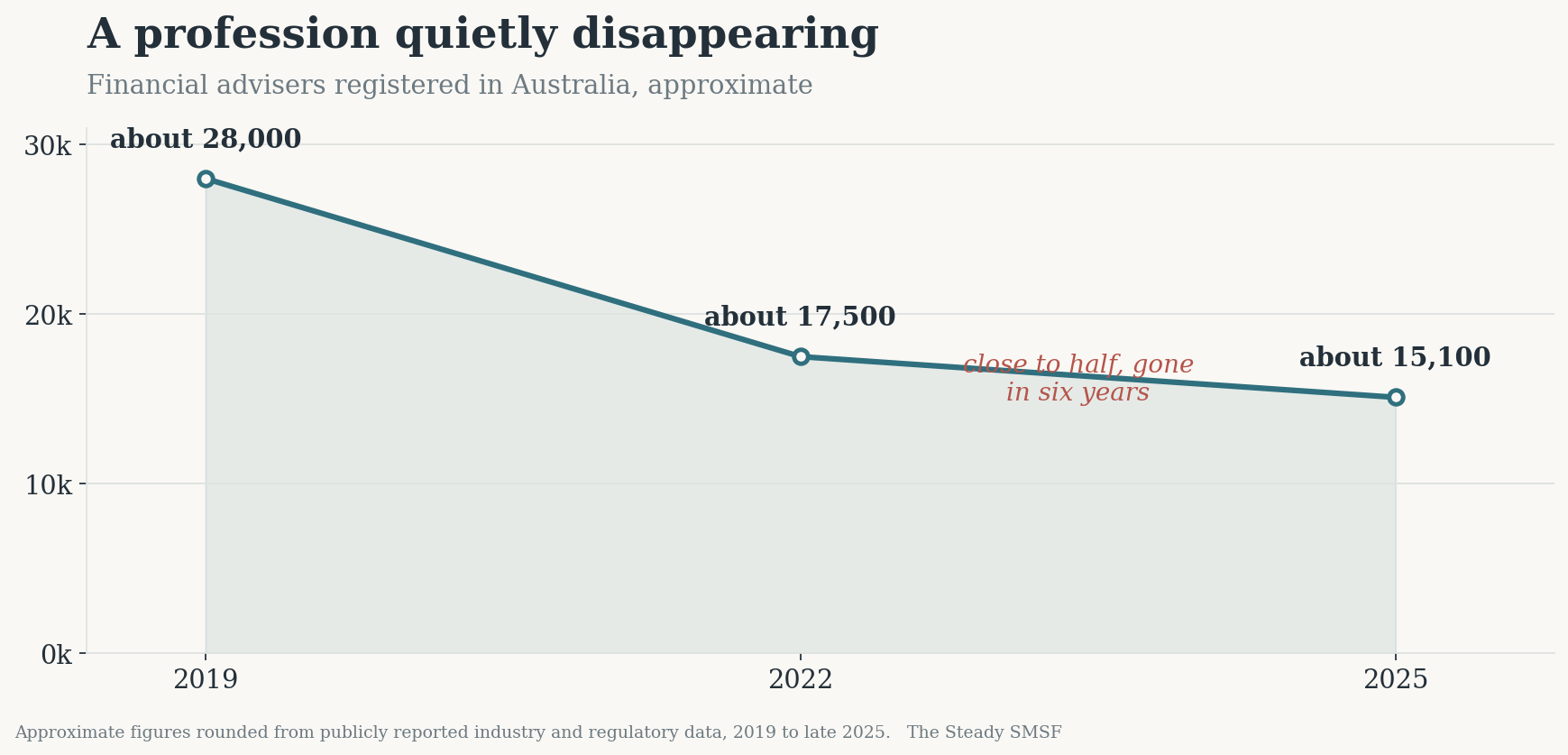

🏚️ A profession that is quietly disappearing

There is another reason this matters more every year. Australia has far fewer advisers than it used to. The number fell from about 28,000 in 2019 to about 15,000 by late 2025, and more left at the end of that year when a new education deadline took effect.

The advisers’ own industry body says nearly 16 million Australians now have advice needs that are going unmet.

What does that mean for you? Advice is harder to find. The advisers who remain are chasing wealthier, more complex clients. Fees keep climbing.

For many trustees, doing it yourself is no longer the odd choice. It is becoming the normal one. Which means doing it well is not optional anymore. It is the job, and it is yours.

🛠️ The advantages of doing it yourself

Put the fees aside for a moment, because the case for doing it yourself is bigger than the money.

You remove a layer between yourself and your money. Every decision is yours, made when you want, with no one to wait on and no one to chase.

Your interests and your choices line up perfectly, because there is no one else in the room with a different motive.

You can also keep things simple. A lot of fancy portfolio design exists just to look worth the fee.

A low-cost, well-spread portfolio that you rarely touch is cheaper to run yourself, and it is often better, because there is less to fiddle with and less to get wrong. The do-it-yourself investor who does very little, on purpose, often beats the advised one who is nudged to do more.

🧠 The reward that never shows up on a bill

Now the part that matters most.

The biggest reward of running your own fund is not the fee you save. It is the person you become by doing the work.

And that person is far harder to fool, to frighten, or to rob than the one who handed it all over.

Think about what doing the work does to you. Once you have read a product disclosure statement yourself, no one can sell you a fairy tale about it.

Once you understand why your portfolio is built the way it is, a market crash stops feeling like the end of the world and starts feeling like something you already planned for.

Once you know what a normal return looks like, anyone promising double that gives themselves away in a single sentence. Doing the work is exactly what makes you impossible to con.

No fee can buy you this. An adviser can hold your portfolio. An adviser cannot give you a steady stomach at the bottom of a crash. That steadiness only comes from doing the reading, making the calls, and living through a downturn with your own money on the line, then watching it recover.

Do that once, and you are changed for good. You become someone who cannot be panicked and cannot be rushed.

Here is the simplest way to say it. An advised investor is buying a portfolio. A do-it-yourself investor, doing it properly, is building a skill.

Only the skill is still standing when the adviser is out of reach, the market is falling, and the decision has to be made tonight, by you.

⚠️ The honest disadvantages

We would be no better than the spruikers if we only sold you the good parts.

Doing it yourself means you are also your own biggest risk. The steadying hand a good adviser provides is real, and without one, you have to be that hand yourself. That is exactly the strength we want to help you build, but it does not come for free. A trustee who panics alone can do more damage in one afternoon than years of fees ever could.

You will also have blind spots. You do not know what you do not know, and super punishes confident mistakes. The work is real work. Hours of reading.

Keeping good records. And the honesty to spot the rare decision that is truly beyond you, then pay for help on that one thing instead of pushing on out of pride. Cheap and wrong costs far more than expensive and right.

The point is not that doing it yourself is free. It is that the price is effort and learning, not a percentage. And unlike a percentage fee, effort and learning pay you back for the rest of your life.

💡 The steady takeaway

The real choice was never adviser against do-it-yourself. Put that way, it is just two camps shouting, and that helps no one decide anything.

The real choice is this. Do you want to understand your own fund, or hand that understanding to someone else and simply hope? You can do the work yourself and still pay, now and then, for real help on the genuinely hard questions.

What you should never do is lean on an adviser so completely that you never learn your own money, because that understanding is the very thing that protects you when no one else is there.

So do the work. Not mainly to save the fee, though you will. Do it because every hour you spend learning your own money turns you into a trustee who cannot be panicked, cannot be rushed, and cannot be sold a bad deal.

That is the best protection money cannot buy, and the one part of all this that is yours to keep forever.

You have already done the brave part. You took the wheel. Now keep learning how to drive, because the more you understand, the steadier you become, and the harder it is for anyone to take what you have built.

Start with one thing this week. Pick one part of your own fund you have always skimmed past: the fees, the holdings, the strategy. Sit with it until you truly understand it. Then do the same with something else next week.

That is how a confident trustee is made. One steady hour at a time.

Steady on.

If this was useful, share it with a friend, a colleague, or someone who has just started their own fund.

The clearer people are about what they can do themselves and what is genuinely worth paying for, the better decisions they make. That is worth spreading.

New here? Start with our free checklist, 10 Questions to Ask Before You Trust Any Investment. It is the most useful thing we can hand you on day one.

The Steady SMSF publishes general information and commentary for self-directed superannuation investors. It is educational in nature and does not constitute personal financial, tax, or legal advice, and does not take into account your objectives, financial situation, or needs. Fee figures and adviser numbers are drawn from publicly reported 2025 industry and regulatory sources and will vary over time and by individual circumstance. Before acting on anything you read here, consider whether it is appropriate for you and seek advice from a licensed professional.

Sources and further reading

On the cost of advice

Canstar, on the cost of a financial adviser, drawing on the Australian Financial Advice Landscape report: canstar.com.au

My Wealth Solutions, reporting the 2025 median ongoing advice fee of about $4,668 from the Australian Financial Advice Landscape report: mywealthsolutions.com.au

For independent, plain-English guidance on advice and its costs, ASIC’s Moneysmart at moneysmart.gov.au is the standard reference.

On the shrinking number of advisers

The Conversation, on the fall in adviser numbers and the reforms behind it: theconversation.com

CPA Australia’s In The Black, on the near-halving of the profession since 2018: intheblack.cpaaustralia.com.au

Independent Financial Adviser (IFA), on the wave of departures around the January 2026 education deadline: ifa.com.au

On unmet advice needs

Small Caps, reporting the Financial Advice Association Australia’s estimate of close to 16 million Australians with unmet advice needs: smallcaps.com.au

Figures are as reported in 2025 and will change over time.